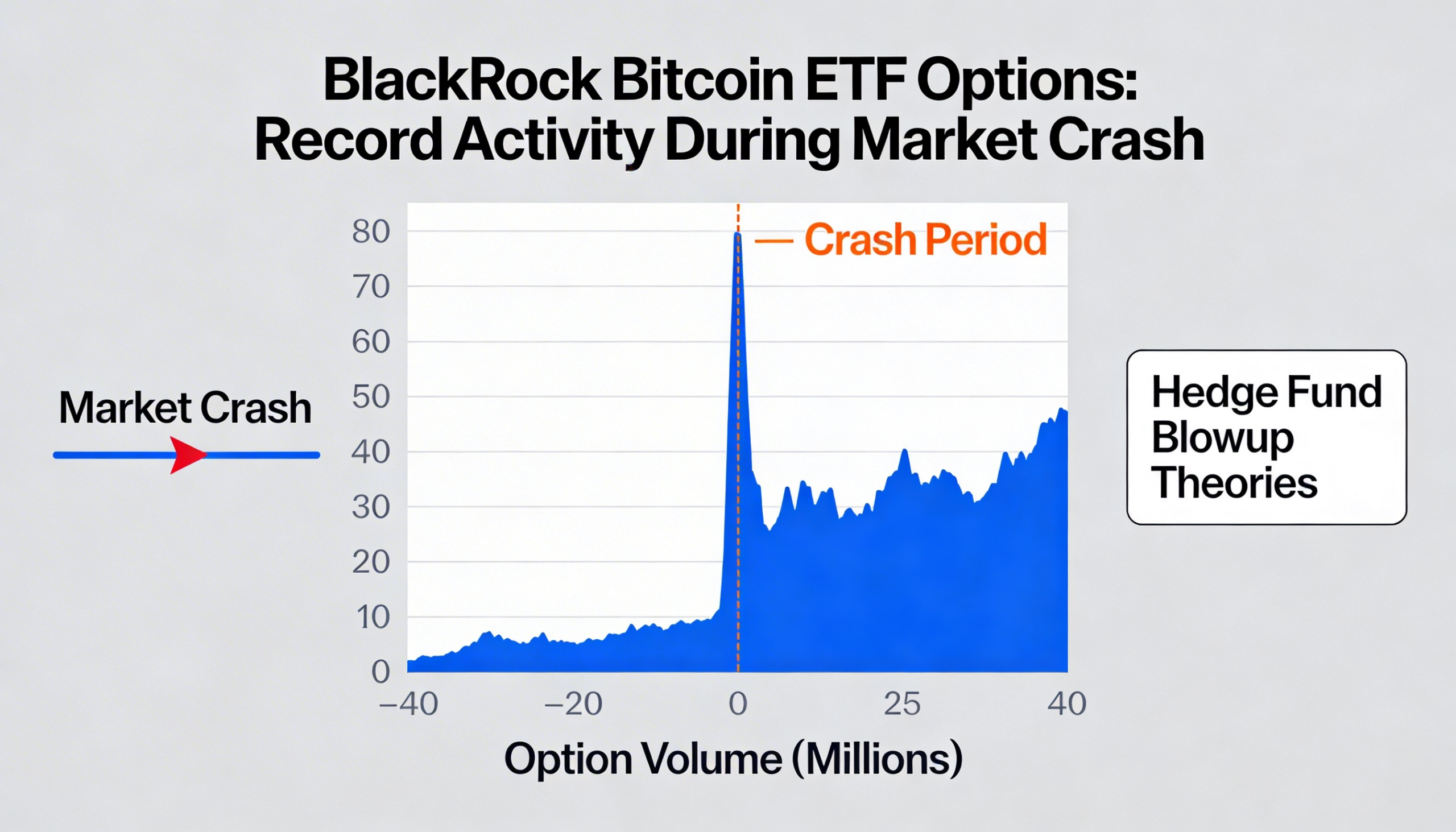

Unprecedented activity in BlackRock’s Bitcoin ETF options amid the crash is raising questions about a possible hedge fund implosion.

Options tied to BlackRock’s spot bitcoin ETF, IBIT, surged to record trading levels last week as bitcoin sold off sharply, sparking debate over whether a hedge fund liquidation amplified the downturn.

Since its launch, IBIT has attracted billions of dollars from investors seeking bitcoin exposure without directly holding the cryptocurrency. Market participants typically monitor fund inflows to assess institutional sentiment, but the latest selloff has shifted attention to options activity as a key indicator.

During Thursday’s decline, IBIT options volume climbed to an all-time high of 2.33 million contracts. By Friday, the ETF had fallen 13% to its lowest level since October 2024. Put options slightly outpaced calls, reflecting increased demand for downside protection, a common feature of stressed markets.

Options allow traders to hedge risk or take leveraged positions with limited downside. Call options offer upside exposure if prices rise above a set level, while put options provide protection if prices fall below it, with losses limited to the premium paid.

Another notable data point was the roughly $900 million in premiums paid by IBIT options buyers that day, the largest single-day total on record and a figure comparable to the market capitalizations of many mid-tier cryptocurrencies.

Liquidation theory gains attention

Speculation intensified after market analyst Parker argued in a widely shared post on X that the record activity reflected the collapse of one or more hedge funds heavily concentrated in IBIT. According to the theory, the fund had built large positions in out-of-the-money call options following the October pullback, betting on a rapid rebound.

Those positions were reportedly financed with leverage. As IBIT continued to decline, the options lost value, triggering margin calls. Unable to meet collateral demands, the fund was allegedly forced to sell large quantities of IBIT shares, contributing to roughly $10 billion in spot trading volume. At the same time, the fund may have rolled or closed expiring options, pushing premium payments to record levels.

Shreyas Chari, director of trading and head of derivatives at Monarq Asset Management, said the selling appeared consistent with margin-driven liquidations.

“Systematic selling across the majors yesterday was probably tied to margin calls, especially in the ETF with the highest crypto exposure, IBIT,” Chari said, adding that rumors circulated of an options-focused entity selling aggressively as key price levels broke.

Others see typical market stress

Some market participants remain unconvinced that a single hedge fund failure explains the surge. Tony Stewart, founder of Pelion Capital, said IBIT options likely contributed to volatility but described the liquidation theory as inconclusive.

Citing data from Amberdata, Stewart said about $150 million of the $900 million in premiums came from traders buying back put options they had previously sold. As IBIT fell and those puts rose sharply in value, traders moved to close positions to limit losses—behavior typical during sharp selloffs.

Stewart added that the remaining premium activity appeared to be spread across smaller trades, consistent with a broadly panicked market. While he acknowledged some activity could have occurred in opaque over-the-counter markets, he said the available data does not definitively point to a single forced liquidation.

Whether driven by hedge fund distress or widespread risk-off positioning, the episode highlights the growing influence of ETF options on crypto market volatility and the increasing importance of derivatives data in assessing institutional behavior.

Share this content: