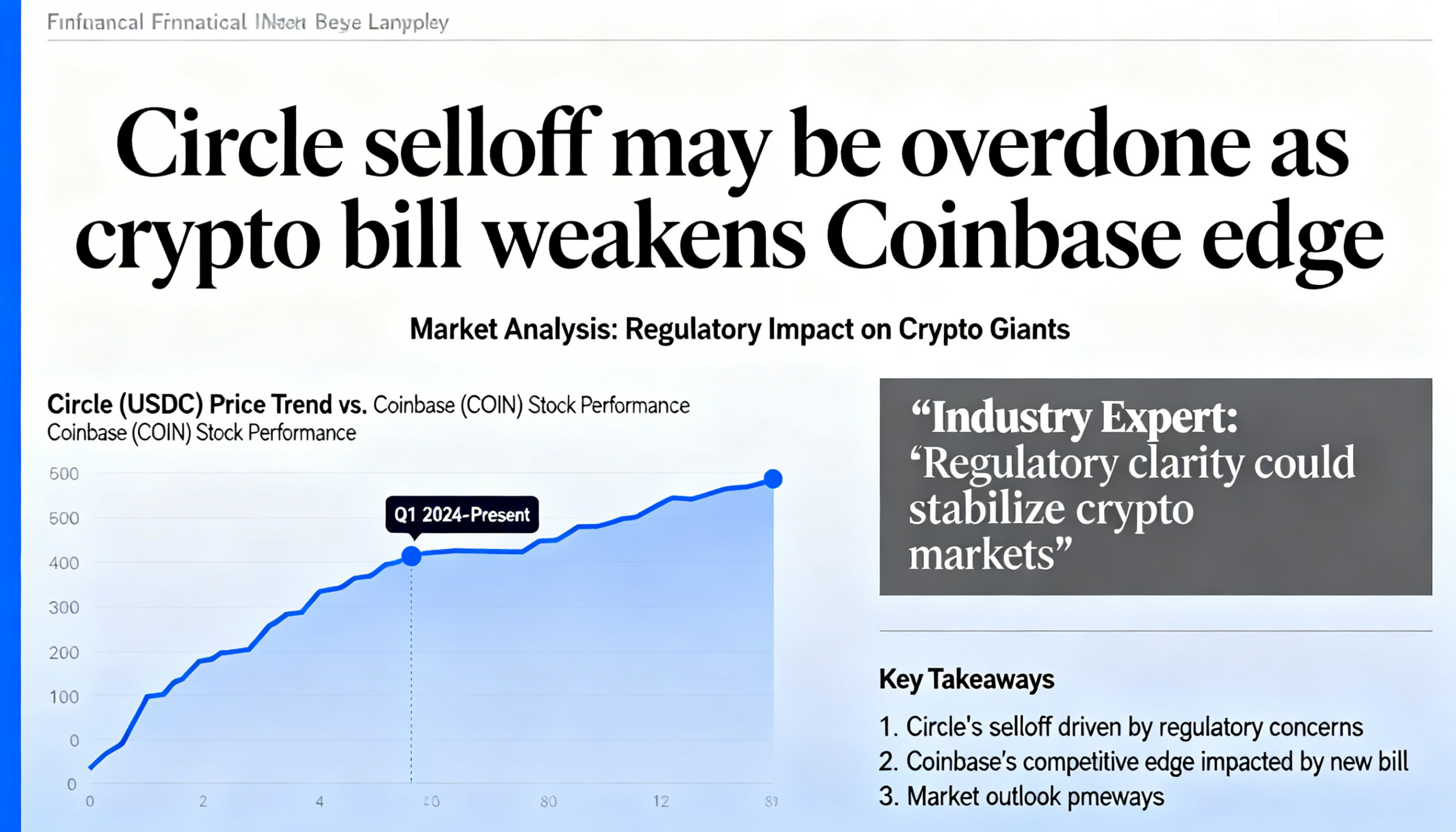

Analysts say Circle’s selloff could be excessive as new crypto legislation erodes Coinbase’s competitive advantage

The latest draft of the CLARITY Act triggered a sharp selloff in both Circle (CRCL) and Coinbase (COIN), but some analysts believe the market reaction may be misreading the longer-term impact of the proposed regulation.

Circle shares took a significantly larger hit than Coinbase on Tuesday following new language around stablecoin yield. While both stocks saw a modest rebound on Wednesday, they remain well below levels seen before the news surfaced earlier in the week.

According to Markus Thielen, founder of 10x Research, the current structure of the bill could ultimately tilt the balance of power in Circle’s favor. He argues that the legislation may weaken Coinbase’s distribution-driven model more than it affects Circle’s role as a stablecoin issuer.

At present, Coinbase captures a substantial portion of the economics tied to USDC through its partnership with Circle. The exchange earns nearly all interest income on USDC held on its platform, while revenue from off-platform balances is typically split evenly. Thielen estimates Circle pays Coinbase over $900 million annually through this arrangement—accounting for roughly half of Circle’s total revenue.

This structure has made stablecoin-related income highly lucrative for Coinbase. However, if regulators move to restrict yield-like incentives on stablecoin balances, that advantage could diminish.

Thielen believes such changes would increasingly benefit Circle, as regulatory clarity could favor issuers with strong compliance frameworks, scale, and robust balance sheets. He also notes that this dynamic may become particularly important ahead of the companies’ next commercial renegotiation, scheduled for August 2026, where Circle could be in a stronger position to secure improved terms.

Meanwhile, Bitwise CIO Matt Hougan views the recent decline in Circle’s stock as overdone, arguing that the CLARITY Act does not undermine the long-term fundamentals of the business.

Hougan points out that yield has never been the primary driver behind stablecoin adoption. Instead, stablecoins have grown rapidly due to their utility in enabling cross-border payments, facilitating trading, and providing access to blockchain-based financial infrastructure. In this context, limiting yield is unlikely to materially impact demand.

He also highlights projections suggesting the stablecoin market could expand to between $1.9 trillion and $4 trillion by the end of the decade. As a leading regulated issuer, Circle could benefit disproportionately if activity continues shifting toward compliant, onshore platforms.

Additionally, Hougan notes that regulatory changes limiting yield passthrough may allow Circle to retain a larger share of its revenue, potentially boosting margins over time.

Taken together, he sees a pathway for Circle to achieve a significantly higher valuation—potentially reaching around $75 billion, or roughly double its current level.

“If stablecoins evolve as expected,” Hougan said, “even conservative assumptions suggest Circle remains an attractive opportunity.”

Share this content: